4.9.3.35 Means test assessment of asset-tested income streams (lifetime)

Summary

This topic covers:

- income test assessment for asset-tested income streams (lifetime)

- assets test assessment for asset-tested income streams (lifetime)

- limits for high surrender values or death benefits.

Note: Grandfathering provisions are applied to lifetime income streams purchased before 1 July 2019, which are assessed as asset-tested income streams (long term).

Overview

The table below gives an overview of the assets and income test treatment of different types of asset-tested income streams (lifetime).

| Type | Assets test | Income test |

|---|---|---|

|

Purchased with superannuation monies |

BEFORE the assessment day, there is no assessable asset value. ON OR AFTER the assessment day, but UP TO AND INCLUDING the threshold day, 60% of the purchase amount is assessed as an asset. AFTER the threshold day, 30% of the purchase amount is assessed as an asset. Asset value may be higher if the income stream has a high surrender value or death benefit. |

60% of the gross payments is assessed as income. |

|

Purchased with non-superannuation monies |

BEFORE the assessment day 100% of the purchase amount is assessed as an asset. ON OR AFTER the assessment day, but UP TO AND INCLUDING the threshold day, 60% of the purchase amount is assessed as an asset. AFTER the threshold day, 30% of the purchase amount is assessed as an asset. Asset value may be higher if the income stream has a high surrender value or death benefit. |

BEFORE the assessment day, the purchase amount is a financial investment and the deeming provisions apply (4.4). ON OR AFTER the assessment day, 60% of the gross payments is assessed as income. |

Income test assessment of asset-tested income stream (lifetime)

Before the assessment day (1.1.A.280) in relation to the income stream:

- if the income stream was purchased with superannuation monies - no income is assessed, as regular payments have not yet commenced

- if the income stream was purchased with non-superannuation monies - the income stream is a managed investment and deemed under the deeming provisions (4.4).

On or after the assessment day in relation to the income stream, 60% of gross payments from an asset-tested income stream (lifetime) is assessed as income.

For deferred income streams (that is, income streams that do not make payments for a set period of time after purchase), income is only assessed when the income stream is making payments (that is, after the deferral period).

Example: Tom receives an annual payment of $5,000 from his lifetime income stream. 60% ($3,000) is assessable income. As his payments increase due to indexation, 60% of the payments will continue to be assessed under the income test for the duration of the lifetime income stream.

Act reference: SSAct section 1099DAB Income—asset-tested income stream (lifetime), section 1120AA Value of asset-tested income streams (lifetime) that are managed investments, section 1120AB Value of asset-tested income streams (lifetime) that are not managed investments

Policy reference: SS Guide 1.1.A.280 Assessment day

Assets test assessment of asset-tested income stream (lifetime)

Before the assessment day in relation to the income stream:

- if the income stream was purchased with superannuation monies - no asset value is assessed. This is consistent with the treatment of other superannuation investments held by a person prior to retirement.

- if the income stream was purchased with non-superannuation monies - the income stream is a managed investment and the full purchase amount (1.1.P.495) is assessed. This is consistent with the treatment of financial investments held by a person outside of superannuation prior to retirement.

On or after the assessment day in relation to the income stream, up to and including the threshold day for the income stream, 60% of the purchase amount of the asset-tested income stream (lifetime) is assessed, provided the income stream does not have high surrender values or death benefits (see below).

After the person's threshold day, 30% of the purchase amount will be assessed for the remaining duration of the lifetime income stream, provided the income stream does not have high surrender values or death benefits (see below).

If the income stream has a surrender value or death benefit above the limits outlined below in any current or future year, then the assessable asset value is the higher of:

- 60% or 30% of the purchase amount (as outlined above)

- the highest surrender value above the limits outlined below on the current and any future day, and

- the highest death benefit above the limits outlined below on the current and any future day.

Note: Deferred income streams are assessed under the assets test from the assessment day. This can include the income stream being assessed under the assets test in the deferral period where payments commence after the assessment day.

Example: Tiffany purchases a lifetime income stream at age 70 (birthday 20 March 1949) on 1 July 2019.

- The assessment day for the income stream is 1 July 2019.

- The threshold day for the income stream is the day before Tiffany's 84th birthday, which is 19 March 2033.

- The purchase amount for the income stream is $200,000.

- The income stream has surrender values and death benefits beneath the limits.

Initially, 60% of the purchase amount ($120,000) is assessed under the assets test. 60% continues to be assessed until 19 March 2033. From 20 March 2033, 30% ($60,000) of the purchase price is an assessable asset. 30% is then assessed for the rest of the duration of Tiffany's lifetime income stream.

Example: Tamara purchases a deferred lifetime income stream at age 83 on 1 July 2019.

- The assessment day for the income stream is 1 July 2019.

- The threshold day for the income stream is the last day of a 5-year period starting on the assessment day, which is 30 June 2024.

- The purchase amount for the income stream is $200,000.

- The income stream has a deferral period of 2 years.

- The income stream has surrender values and death benefits beneath the limits.

Initially, 60% of the purchase amount ($120,000) is assessed under the assets test. 60% continues to be assessed until 30 June 2024. From 1 July 2024, 30% ($60,000) of the purchase price is an assessable asset. 30% is then assessed for the rest of the duration of Tamara's lifetime income stream. The deferral period for Tamara's lifetime income stream does not impact her assets test assessment.

Act reference: SSAct section 1120AA Value of asset-tested income streams (lifetime) that are managed investments, section 1120AB Value of asset-tested income streams (lifetime) that are not managed investments

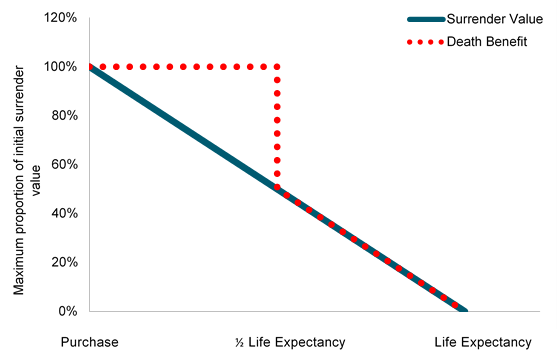

Limits for high surrender values or death benefits

The assets test rules for asset-tested income streams (lifetime) have additional provisions for products with surrender values or death benefits above the limits imposed by the Capital Access Schedule in the Superannuation Industry (Supervision) Regulations 1994.

The limits are outlined in the following graph:

This graph outlines the limits applied to lifetime income streams under the Capital Access Schedule at different ages, based on a person's life expectancy. At purchase, the surrender value limit is 100% of the initial surrender value. This decreases on a straight-line basis to life expectancy. That is, at half-way to life expectancy, the surrender value is half (50%) of the initial surrender value, and at life expectancy the surrender value limit is zero. The death benefit limit is 100% of the initial surrender value at purchase. It is 100% of the initial surrender value up until half-life expectancy, at which point the death benefit limit drops to 50%. The death benefit limit then reduces on a straight line basis to life expectancy, when the death benefit limit is zero.

On a given day (the access day), the limit for surrender values is:

- for a day during the 14-day period that begins on the assessment day for the income stream: the access amount (exclusive of the assessment day)

- for any other day, the greater of nil or the amount worked out using the following formula:

- ((access amount ÷ life expectancy period for the income stream) × remaining life expectancy) − any commuted amounts.

On a given day (the access day), the limit for death benefits is:

- for a day during the first half of the life expectancy period for the income stream: the access amount

- for any other day, the greater of nil or the amount worked out using the following formula:

- ((access amount ÷ life expectancy period for the income stream) × remaining life expectancy) − any commuted amounts.

Where:

- access amount-the maximum amount that would have been payable for the income stream, as determined by the contract or governing rules for the income stream, if the income stream had been commuted on the assessment day for the income stream, plus any instalments paid for the income stream after the assessment day and before the access day

- life expectancy period - the number of days

- using the life tables (4.9.5) to calculate the number of days, at the assessment day, in the life expectancy of

- the person eligible to receive the income stream, or

- for a joint income stream-the eldest of those eligible to receive the income stream, and

- rounding that number of days down to the nearest whole number of years, and

- converting those years to a number of days, assuming 365 days in a year

- using the life tables (4.9.5) to calculate the number of days, at the assessment day, in the life expectancy of

- remaining life expectancy means the number of days remaining in the life expectancy period for the income stream after subtracting the number of days in the period

- starting on the assessment day for the income stream (exclusive of the assessment day), and

- ending on the access day.

Example: Tamotsu purchases an asset-tested income stream (lifetime) at age 70 (birthday 20 September 1949) on 1 January 2020.

- The assessment day for the income stream is 1 January 2020.

- The threshold day for the income stream is the day before Tamotsu's 84th birthday, which is 19 September 2033.

- Tamotsu's life expectancy period is 15 years (5,475 days).

- The purchase amount for the income stream is $200,000.

- The access amount for the income stream is $200,000.

- The income stream has no surrender value until Tamotsu turns 80. While Tamotsu is 80, the income stream has a surrender value of $200,000. From when Tamotsu turns 81, the income stream has no surrender value again.

- The income stream has no death benefit.

- Tamotsu has made no commutations from the income stream.

For the year when Tamotsu is 80, the income stream has a surrender value. The surrender value limit when Tamotsu is 80 is:

- ($200,000 ÷ 5,475) × 1,925 = $70,319.63

as there are 1,925 days remaining in the life expectancy period (exclusive of the assessment day).

The surrender value of Tamotsu's income stream is $200,000, which is greater than the surrender value limit. For all days before Tamotsu turns 81, the standard assets test assessment is compared against the $200,000 surrender value. The higher value is assessed as an asset.

The assessable value of Tamotsu's income stream is as follows:

- From the assessment day until the day before Tamotsu turns 81 (that is, from 1 January 2020 to 19 September 2029), the income stream has an assessable value of $200,000 (the full future surrender value).

- From 20 September 2029 to the threshold day (19 September 2033), the income stream has an assessable value of $120,000 (60% of $200,000).

- From 20 September 2033 onwards, the income stream has an assessable value of $60,000 (30% of $200,000).

Example: Tegan purchases an asset-tested income stream (lifetime) at age 70 (birthday 1 November 1949) on 1 January 2020.

- The assessment day for the income stream is 1 January 2020.

- The threshold day for the income stream is the day before Tegan's 84th birthday, which is 31 October 2033.

- Tegan's life expectancy period is 18 years (6,570 days).

- The purchase amount for the income stream is $200,000.

- The access amount for the income stream is $200,000.

- The income stream has no surrender value.

- The income stream has a death benefit of $80,000 for the duration of the income stream.

- Tegan has made no commutations from the income stream.

Tegan's income stream has a consistent death benefit of $80,000. This is less than 60% of the purchase amount ($120,000), and will therefore not affect her assessable asset value prior to the threshold day for the income stream.

After the threshold day, the death benefit limit for the income stream is:

- ($200,000 ÷ 6,570) × 1,518 = $46,210.05.

As the death benefit for Tegan's income stream is $80,000, it is greater than the death benefit limit after the threshold day, and also greater than 30% of the purchase amount ($60,000).

This means the assessable value of Tegan's income stream is:

- 60% of $200,000 ($120,000) until Tegan reaches their threshold day (30 October 2033).

- $80,000 (the full current and future death benefit amount) from 1 November 2033 onwards.